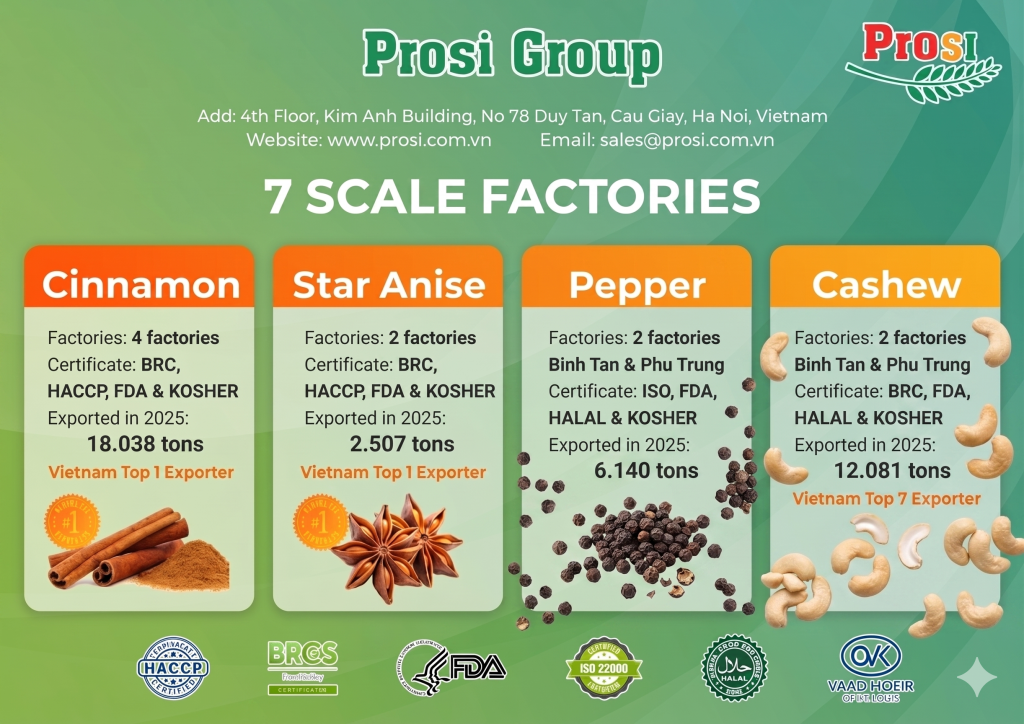

Strategic Resilience and Record-Breaking Milestones: Prosi Group’s 2025 Annual Performance Review

The year 2025 was a definitive “pressure test” for the global agricultural trade. For Prosi Group, it was a period characterized by a “perfect storm” of logistical bottlenecks, shifting geopolitical landscapes, and complex international trade policies. Yet, in the face of these headwinds, our commitment to operational excellence allowed us to not only navigate the turbulence but to emerge with a historic, record-breaking performance.

For our valued partners and brokers, this report details how we transformed a challenging global environment into a year of unprecedented growth and reliability.

Navigating the Global “Pressure Test”

The 2025 fiscal year was marked by several external disruptions:

- Geopolitical & Tax Shifts: The implementation of US countervailing duties and evolving international tax frameworks required immediate strategic agility.

- Logistical Complexity: Global shipping constraints and rising transit costs tested the limits of “just-in-time” supply chains.

- Domestic Restructuring: Vietnam’s internal administrative shifts and province mergers created a new landscape for regional sourcing and documentation.

Despite these hurdles, Prosi Group leaned into its core strength: The Farm-to-Port Model. By maintaining direct control over our supply chain, we ensured that the “spice flow” remained uninterrupted for our clients worldwide.

A Year of Vertical Growth: Sector Highlights

Our success in 2025 was driven by a diversified approach across our four core pillars, with each sector achieving significant milestones:

1. Cinnamon (Cassia) & Star Anise: Defending the Crown

As the cornerstone of our spice division, we successfully defended our position as Vietnam’s Top 1 Exporter for both products.

- Cinnamon: We reached a total volume of 18,038 tons, a robust 19% increase over 2024. Our ability to secure premium raw materials despite regional weather volatility ensured we remained the primary choice for global brokers.

- Star Anise: In an increasingly competitive regional market, we remained the undisputed leader, exporting 2,507 tons characterized by high essential oil content and visual purity.

2. Cashews: The Strategic Breakout

The standout performer of 2025 was our cashew division. We witnessed an explosive 84% growth (+3,582 tons), reaching a total of 12,081 tons. This surge propelled Prosi Group into the Top 7 Cashew Exporters in Vietnam, a testament to our recent investments in high-tech processing and BRC-compliant quality control.

3. Pepper: Resilience Against Trade Barriers

Despite the significant headwinds posed by the US countervailing duty policies, our pepper exports reached 6,140 tons—a 4% increase. By diversifying our market reach and focusing on high-quality white and black pepper, we provided our partners with a stable supply route even when trade barriers were at their highest.

Operational Excellence in Numbers

At our operational peak in 2025, Prosi Group managed the seamless transit of 256 containers per month. This logistical feat was supported by our seven state-of-the-art factories, ensuring that every container met the most stringent international standards.

This relentless focus on execution resulted in a historic annual revenue of $181 million USD (over 4.59 trillion VND).

Quality Compliance: Our Global Passport

We understand that for our international clients, reliability is built on certification. Throughout 2025, we maintained and renewed our rigorous audit-ready status across all major benchmarks:

- BRC Global Standard (Grade A): Ensuring the highest food safety protocols.

- Kosher (Pareve) & Halal: Providing universal accessibility for diverse consumer markets.

- FDA & ESG Compliance: Aligning with the modern requirements of the North American and European markets.

A Partnership Built on Mutual Trust

To our importers, brokers, and collaborators: This record-breaking year is a shared victory. In a year where logistical delays were the global norm, your patience and continued feedback allowed us to refine our operations. You challenged Prosi Group to be better, and in return, we prioritized your supply security above all else. Your trust provided the foundation upon which these records were built.

Looking Ahead: The 2026 Harvest

As we transition into 2026, the market remains tight, and the “Quality-Driven” era of spice trading is officially here. We invite you to join us as we harvest the results of our 2025 investments. With our enhanced infrastructure and certified quality, Prosi Group is ready to lead your supply chain into a prosperous new year.

Ready to secure your 2026 requirements with Vietnam’s most resilient partner? Contact our export team today.

Vietnam Pepper 2025: A Year of Structural Change and the Foundation for 2026.

The final data for 2025 is in, and it tells a story of a market in profound transition. For global importers and brokers, the takeaway is clear: the era of “cheap and abundant” Vietnamese pepper has been replaced by a new reality of value-driven scarcity. As a leading voice in the Vietnamese spice sector, Prosi Group presents this comprehensive analysis of the 2025 performance and the critical supply-side hurdles awaiting the 2026 cycle.

I. The 2025 Performance: A Historic Financial Milestone

Despite a slight contraction in total export volume, 2025 will be remembered as the year Vietnamese pepper reached its highest financial peak in history.

- The Record Figures: Vietnam exported 247,482 tons, generating a staggering $1.66 billion in revenue. While volume dipped by 1.2% compared to 2024, the export value surged by 26%.

- The Price Revolution: The average export price for Black Pepper hit $6,607/ton (+36.2%) and White Pepper reached $8.629/ton (+33.6%).

- Dominance in Spices: Pepper now accounts for 78.2% of Vietnam’s total spice export value. This confirms that even as we diversify into Cinnamon and Star Anise, Pepper remains the flagship of our agricultural strength.

II. Production Analysis: The Calm Before the 2026 Storm

In 2025, Vietnam maintained its status as the global production hub with 195,000 tons. High prices incentivized farmers to invest in better fertilizers and irrigation, which stabilized yields for the 2025 harvest. However, the outlook for 2026 is significantly more fragile:

- Climatic Hostility: 2025 saw extreme weather patterns. Prolonged droughts in the “Pepper Belt” (Đắk Lắk, Gia Lai, Đắk Nông) followed by unseasonal heavy rains have weakened crop health.

- The Disease Factor: High humidity has triggered outbreaks of root rot and Phytophthora in aging orchards. While young gardens remain productive, they cannot offset the decline in older regions.

- The 2026 Forecast: We estimate a 15-20% reduction in harvest volume, with total output likely dropping to 165,000 tons. This will be the tightest supply window we have seen in years.

III. The Global Pivot: Asia Rises as the West Recalibrates

The flow of Vietnamese pepper underwent a massive geographical re-routing in 2025, reflecting broader macroeconomic shifts:

- Asia Takes the Lead: Now commanding 47.4% of total exports (up from 38% in 2024). This growth was propelled by a 35.6% surge in UAE intake and an 88% rebound in Chinese demand. These markets are increasingly acting as hubs for re-processing and regional distribution.

- The Western Retreat: Exports to the Americas dropped by 22.7% and Europe by 13.1%. High interest rates in the US and EU forced many buyers to work through existing inventories (destocking) rather than buying at peak 2025 prices.

- The VAT Catalyst: With the Vietnamese government recently abolishing VAT on export items, domestic enterprises now have a significant liquidity boost to accelerate shipments in early 2026.

IV. Strategic Forecast: What Importers Must Know for 2026

As we approach the 2026 harvest (expected to begin in late February), the “wait for a price drop” strategy may be highly risky.

- Farmer Psychology: Vietnamese farmers are now financially robust. Strong profits from Coffee, Durian, and the 2025 Pepper cycle mean they are under zero pressure to sell ồ ạt (mass-sell). They will release stock slowly and strategically to maintain price levels.

- Inventory Scarcity: Carry-over stock into 2026 is estimated at just 40,000 tons. With global demand consistently high and other origins (except Brazil) also seeing production drops, the global supply gap is widening.

- A New Price Floor: We anticipate that the 2025 prices were not a temporary spike but the establishment of a new price floor. —

The Prosi Group Conclusion

At Prosi Group, we believe 2026 will be a year defined by sourcing security. In a market where volume is shrinking and farmers have the financial power to hold stock, “price hunting” will likely lead to missed opportunities and supply chain disruptions.

The industry leaders—Olam, Phuc Sinh, and the Prosi network—are already aligning with a more structured, long-term procurement model. We advise our global partners to move away from spot-market volatility and toward strategic partnerships to ensure continuity for the 2026 season.

Is your supply chain resilient enough to handle a 20% drop in global availability? Connect with the experts at Prosi Group to secure your Q1 and Q2 2026 requirements.

Vietnam Star Anise 2025: A Year of Price Resilience and Strategic Pivot

The 2025 fiscal year has drawn to a close, leaving behind a complex but promising trail for the Vietnamese Star Anise industry. As a global leader in this sector, Prosi Group provides a deep dive into the shifts in volume, pricing volatility, and the emerging dominance of premium markets that defined the past 12 months.

📊 The Macro View: Volume Stability vs. Value Compression

According to the latest VPSA data, Vietnam’s Star Anise exports reached 14,307 tons in 2025. While this represents a modest 2.2% growth in volume compared to 2024, the total export turnover settled at $58.7 million—an 8.0% decline in value.

The narrative of 2025 was one of “Value Correction.” After the high-price cycles of previous years, the market faced downward pressure due to increased regional competition and a temporary slowdown in global industrial demand during the first three quarters.

📈 The “Year-End Rally”: A Q4 Pricing Surge

The most compelling story of 2025 lies in the final quarter. While the annual average price dipped to $4,237/ton (down 11.2% from 2024), Q4 witnessed a spectacular recovery:

- October: $4,991/ton (+12.1% YoY)

- November: $5,034/ton (+11.4% YoY)

- December: $4,546/ton (+26.0% YoY)

This late-year momentum signals a tightening of high-quality supply and a robust restocking phase from major global buyers entering 2026.

🌍 Market Footprint: The “India Anchor” & The “American Surge”

Vietnam’s Star Anise remains highly concentrated, yet strategically expanding:

- India (The Anchor): Remains the undisputed central hub, absorbing 9,896 tons (69.2% market share). India’s 5.8% growth confirms its role as the world’s primary processing and consumption engine for Star Anise.

- USA (The Growth Engine): In a landmark shift, exports to the United States skyrocketed by 82.9%, reaching 1,030 tons. This reflects a growing appetite in the West for high-essential-oil-content Star Anise for the pharmaceutical and premium F&B sectors.

- Emerging Frontiers: Remarkable triple-digit growth in markets like Pakistan (+306%) and Peru (+193%) suggests that Vietnamese Star Anise is successfully penetrating new culinary and industrial geographies.

🏆 Competitive Landscape: Prosi Thăng Long Leads the Charge

Despite a fragmented exporter base, Prosi Thăng Long has officially secured its position as the #1 Star Anise Exporter in Vietnam, commanding a 16.6% market share with 2,374 tons.

In a year defined by price sensitivity, our strategy focused on Execution Excellence and Quality Consistency. While some segments of the market faced volume retreats, Prosi Group maintained its lead by bridging the gap between local farming cooperatives and the stringent standards of our global partners.

🧭 The 2026 Strategic Outlook

The data from 2025 presents a clear mandate for the industry: Diversification and Value-Add.

- Reducing Over-reliance: While India remains vital, the surge in the USA and EU markets proves that quality-driven buyers are willing to pay a premium for certified, traceable Star Anise.

- Climate & Compliance: As supply chains become more transparent, Prosi Group is doubling down on ESG-compliant sourcing to navigate the evolving “Green” regulations in premium markets.

Final Thought: 2025 was a foundation-building year. The price rally in December suggests that 2026 will be a year of high demand and strategic sourcing.

Are you ready to secure your Star Anise supply chain for the 2026 cycle? Connect with Prosi Group—the trusted leader in Vietnamese Spices.

Scaling the Summit: Vietnam’s Cinnamon Export Dominance in 2025

As we close the books on 2025, the data confirms a transformative shift in the global spice trade: Vietnam has solidified its position as the undisputed “Spice King” of the Cinnamon market. For global importers and brokers, understanding the 2025 momentum is critical for navigating the supply chain complexities of 2026. At Prosi Group, we have analyzed the year-end figures to provide you with a strategic roadmap for the months ahead.

1. The Q4 Momentum: A Masterclass in Resilience

After a challenging third quarter, the market witnessed an extraordinary V-shaped recovery.

- The December Surge: Exports reached 11,366 tons in December, a sharp +20.07% increase from November. This marked the third consecutive month of growth, driven by peak holiday demand in the West and Lunar New Year restocking in Asia.

- A New Baseline: The year concluded with a total volume of 120,295 tons. To put that in perspective, 2025 outperformed 2024 by ~19% and 2023 by a staggering ~35%.

The Takeaway: Global reliance on Vietnamese Cassia is no longer seasonal; it is a structural preference over other origins like Indonesia or Sri Lanka.

2. Global Market Shift: The Rise of the “Trade Hubs”

While traditional markets remain strong, 2025 revealed a fascinating shift in how Cinnamon flows across the globe:

- The “Big Three” Backbone: India (37.6% share), the USA (11.3%), and Bangladesh (8.5%) remain the primary engines of demand. India alone absorbed over 45,000 tons, reclaiming its role as the dominant consumer and processor.

- The Hub Strategy: We saw explosive growth in transit hubs. Singapore surged by +364% and UAE by +108%. This indicates that international traders are increasingly using these hubs to manage logistics and financial hedging before redistributing to final destinations.

- The China Rebound: After a period of stagnation, demand from China skyrocketed by +147%, likely due to a domestic supply gap and a shift toward higher-quality Vietnamese imports.

3. The 2026 Landscape: Red Sea, EUDR, and Strategic Sourcing

As we transition into 2026, the “Golden Age” of Vietnamese Cinnamon faces a more complex regulatory and logistical environment:

- Logistics Alert: Continued tensions in the Red Sea mean longer transit times (10-14 days extra) and elevated ocean freight. Strategy: Buyers must prioritize earlier booking and higher safety stocks.

- The “Green” Filter: With EUDR (European Deforestation Regulation) and ESG mandates taking full effect, 2026 will be the year that separates professional exporters from casual traders. Compliance is no longer an option—it is a ticket to the market.

- Sourcing Trends: The “China + 1” strategy continues to favor Vietnam as global buyers seek stability outside traditional geopolitical zones.

4. Prosi Group: The Market Maker’s Perspective

In a year of record-breaking industry performance, Prosi Group has reached a milestone that redefines leadership:

- Unrivaled Scale: We ended 2025 as the #1 Exporter with 18,028 tons—holding a 15% total market share. Our volume is now 2.5 times larger than our nearest competitor.

- Operational Stability: While many large players saw a -90% dip in December volume due to supply chain fatigue, Prosi remained steady, exporting 1,335 tons (the highest in the market).

- Why it matters to you: Our scale allows us to act as a Market Maker. We offer price stability, guaranteed execution, and the most robust ESG-compliant supply chain in Vietnam.

Conclusion & 2026 Outlook

We forecast 2026 to grow at a more disciplined rate of 8-12%. Quality standards will tighten, and logistical costs will remain a variable. In this environment, the “Prosi Advantage” is your greatest hedge against uncertainty.

To our global partners: Thank you for trusting us through a record-breaking year. To those looking to secure a stable, high-volume supply for 2026—let’s start the conversation today.

Vietnam’s Cinnamon and Star Anise Market Report 2024

I/ Cinnamon: Growth and Market Dynamics

In 2024, Vietnam recorded a total cinnamon export volume of 99,874 tons, generating export revenue of USD 274.5 million, marking an 11.7% increase in volume and a 5.2% increase in value compared to 2023. Despite a 9.4% decline in volume and an 11% decline in value during the first four months of the year, the sector experienced a significant recovery toward the end of 2024.

Export Market Highlights

India remained the largest export market for Vietnamese cinnamon in 2024, with 35,885 tons exported, accounting for 35.9% of total exports. However, this marked a 5.7% decrease compared to the previous year.

The United States was the second-largest market, with 11,078 tons exported, representing 11.1% of total exports and an impressive 9.0% growth compared to 2023.

Bangladesh ranked third, with 7,928 tons exported, accounting for 7.9% of total exports and achieving a remarkable 42.5% increase year-over-year.

Leading Exporters in 2024

Prosi Thăng Long continued to dominate the cinnamon export sector as the largest exporter in Vietnam, contributing 14.9% of total exports with 14,891 tons, a 7.6% increase compared to 2023.

The following companies also made significant contributions:

- Gia Vị Sơn Hà: Exported 6,163 tons, an impressive 31.8% growth, accounting for 6.2% of the market.

- Tuấn Minh: Exported 4,618 tons, a remarkable 48.3% growth, accounting for 4.6% of the market.

- Senspices Việt Nam: Exported 4,299 tons, a 16.2% decline, accounting for 4.3% of the market.

- Olam Việt Nam: Exported 4,128 tons, a 19.8% growth, accounting for 4.1% of the market.

Prosi Thăng Long’s Leadership

Prosi Thăng Long reaffirmed its position as the industry leader in 2024, maintaining the largest market share in Vietnam’s cinnamon export sector. This achievement reflects the company’s consistent commitment to quality, market expansion, and innovation in the spice industry.

II/ Overview of Star Anise in Vietnam

In 2024, Vietnam exported 14,004 tons of star anise, generating a total export revenue of USD 63.7 million. This represented a 5.7% decline in export volume and a 16.2% drop in value compared to 2023. Despite these challenges, Prosi Thăng Long achieved significant growth, reinforcing its leadership in the star anise export sector.

Export Market Highlights

India remained the largest market for Vietnamese star anise, accounting for 66.8% of total exports, with 9,352 tons exported—an impressive 19.0% growth compared to the previous year.

Other notable export markets included:

- United States: 563 tons

- China: 420 tons

- Taiwan: 361 tons

- Thailand: 269 tons

Leading Exporters in 2024

Prosi Thăng Long solidified its position as the top exporter of star anise in Vietnam, exporting 2,865 tons and accounting for 20.5% of the total market share, a 19.6% increase compared to 2023.

Other key contributors included:

- Tuấn Minh: 769 tons

- Senspices: 579 tons

- Hồng Sơn Việt Nam: 446 tons

- Huy Chúc M & M: 398 tons

Prosi Thăng Long’s Expansion

To meet growing market demand, Prosi Thăng Long expanded its production capacity by opening a new factory in Lạng Sơn in 2024. This strategic move underscores the company’s commitment to innovation and its mission to deliver premium-quality star anise to global markets.

III/ Challenges in Vietnam’s Cinnamon and Star Anise Export Sector

Despite achieving positive results, Vietnam’s cinnamon and star anise industries face numerous challenges that demand strategic solutions to sustain growth and competitiveness in the global market.

1. Intensifying Competition

The global spice market is becoming increasingly competitive, with major exporting countries such as Indonesia, Sri Lanka, and India vying for market share. Vietnamese exporters must differentiate themselves by offering superior quality and value-added products to remain ahead of competitors.

2. Stringent Quality Standards

Importing markets, especially in the EU and the United States, are implementing stricter quality and safety requirements. These include higher standards for pesticide residues, microbiological safety, and organic certifications. Meeting these demands requires significant investments in processing technology, quality control systems, and compliance documentation.

3. Price Volatility

The international market for cinnamon and star anise is highly sensitive to price fluctuations caused by supply-demand imbalances, currency exchange rates, and geopolitical factors. Such volatility poses risks to exporters, particularly when negotiating long-term contracts.

Prosi Thăng Long’s Approach

As the industry leader, Prosi Thăng Long is proactively addressing these challenges by:

- Strengthening Market Relationships: Building strong partnerships with key buyers to navigate market uncertainties effectively

- Investing in Modern Facilities: Expanding production capabilities, such as the new factory in Lạng Sơn, to ensure consistent quality and supply.

- Enhancing Quality Control: Implementing advanced processing technologies to meet stringent international standards.

IV/The Rising Trend of Organic Cinnamon and Star Anise Development

Vietnam has been the world’s largest exporter of cinnamon since 2021, a remarkable achievement that highlights the country’s pivotal role in the global spice industry. To sustain and enhance this position, the cinnamon and star anise sector must embrace innovation, with the development of organic production emerging as a key strategy for the future.

Why Organic Matters

- Global Demand for Organic Products

Consumers worldwide are increasingly prioritizing health, sustainability, and environmentally friendly practices. The demand for organic spices, including cinnamon and star anise, is rising, especially in high-value markets such as the EU, the United States, and Japan. - Enhanced Market Access

Organic certifications open doors to premium markets and allow Vietnamese exporters to secure higher profit margins. Products labeled organic carry a reputation for quality and sustainability, aligning with global trends. - Sustainability and Environmental Benefits

Organic farming practices reduce the use of harmful pesticides and synthetic fertilizers, promoting healthier ecosystems and long-term soil fertility. This ensures sustainable growth for the industry while addressing environmental concerns.

Prosi Thăng Long’s Vision for Organic Spices

As a leader in Vietnam’s spice export industry, Prosi Thăng Long is committed to advancing organic cinnamon and star anise production. Key initiatives include:

- Supporting Farmers: Collaborating with local growers to transition to organic farming practices, providing technical training, and ensuring compliance with international organic standards.

- Investing in Certification: Achieving globally recognized organic certifications to boost the marketability of Vietnamese spices.

- Promoting Sustainability: Implementing eco-friendly practices across the supply chain to reinforce Vietnam’s reputation as a responsible and sustainable supplier.

The Road Ahead

The development of organic cinnamon and star anise represents a critical step in securing Vietnam’s position as a global leader in the spice market. By embracing this trend, the industry can not only meet evolving consumer preferences but also contribute to a more sustainable and resilient future for Vietnamese agriculture.

#ProsiThangLong#Prosi#GlobalTrade#VietnamSpices#VietnamNuts#Pepper#Cashew#Cinnamon#Coconut#StarAnise#VietnamExporter

——————————-

𝐏𝐫𝐨𝐬𝐢 𝐓𝐡𝐚𝐧𝐠 𝐋𝐨𝐧𝐠 – 𝐒𝐩𝐢𝐜𝐞𝐬 𝐚𝐧𝐝 𝐍𝐮𝐭𝐬 𝐕𝐢𝐞𝐭𝐧𝐚𝐦 𝐌𝐚𝐧𝐮𝐟𝐚𝐜𝐭𝐮𝐫𝐞𝐫 𝐚𝐧𝐝 𝐄𝐱𝐩𝐨𝐫𝐭𝐞𝐫

![]() 𝐀𝐝𝐝𝐫𝐞𝐬𝐬: 4th Floor, Kim Anh Building, No 78 Duy Tan, Cau Giay, Ha Noi

𝐀𝐝𝐝𝐫𝐞𝐬𝐬: 4th Floor, Kim Anh Building, No 78 Duy Tan, Cau Giay, Ha Noi

![]() 𝐄𝐦𝐚𝐢𝐥: Sales@prosi.com.vn

𝐄𝐦𝐚𝐢𝐥: Sales@prosi.com.vn

![]() 𝐎𝐟𝐟𝐢𝐜𝐞 𝐇𝐨𝐭𝐥𝐢𝐧𝐞: (+84) 9858 17797

𝐎𝐟𝐟𝐢𝐜𝐞 𝐇𝐨𝐭𝐥𝐢𝐧𝐞: (+84) 9858 17797

𝐘𝐨𝐮𝐫 𝐭𝐫𝐮𝐬𝐭𝐞𝐝 𝐩𝐚𝐫𝐭𝐧𝐞𝐫 𝐢𝐧 𝐩𝐫𝐞𝐦𝐢𝐮𝐦 𝐬𝐩𝐢𝐜𝐞𝐬 𝐚𝐧𝐝 𝐧𝐮𝐭𝐬

Overview of the Vietnamese Cashew Industry

The year 2024 has been a landmark period for Vietnam’s cashew industry, showcasing impressive growth, international collaboration, and strategic advancements in global markets. With continued efforts to enhance quality and diversify export destinations, Vietnam has reinforced its position as the largest exporter of cashews in the world, accounting for over 80% of global market share.

Key Highlights of 2024

1. Exceptional Export Growth

Vietnam achieved remarkable export results, with total export turnover estimated at $3.6 billion, a 7% increase compared to 2023. From January to November, the country exported 711,500 tons of cashews, marking a 22.2% rise in volume and 30.7% growth in value year-over-year.

- USA: Remains the largest market with 147,000 tons exported, generating $866 million (20.6% of total export value).

- China: Secured the second position with imports valued at $616 million (15.06% of total exports).

- European Union and Others: Accounted for 64.33%, equivalent to 457,000 tons, valued at $2.75 billion.

2. Rising Cashew Kernel Prices

Early 2024

The domestic raw cashew price ranged from 28,000 to 32,000 VND/kg, showing a slight increase of 5% compared to the same period in 2023.

Reason: Limited supply caused by a decline in raw cashew production from major producers like India and Côte d’Ivoire.

Mid-2024

The international price of W320 cashew kernels reached $6,900 to $8,100/ton, a strong increase of 10% compared to early 2024.

In Vietnam, W320 cashew kernels were priced at around 130,000 to 135,000 VND/kg, marking the most significant growth in the past three years.

Late 2024

The price of raw cashews slightly decreased to 26,000 to 28,000 VND/kg, as raw cashew imports from Africa resumed.

W320 cashew kernel prices remained stable at high levels, around $7,000 to $7,200/ton, driven by strong demand from the U.S. and EU markets.

Reasons Behind Price Fluctuations

Limited Supply

- Vietnam’s raw cashew production in 2024 is estimated at 420,000 tons, a slight 2% increase from 2023, but insufficient to meet processing demands.

- Major raw cashew exporters like Côte d’Ivoire and Ghana reported lower production due to adverse weather conditions.

Increased International Demand

- Vietnam’s cashew exports to major markets, including the U.S., EU, and the Middle East, saw robust growth.

- Demand for high-quality kernels like W320 and W240 increased by more than 15% compared to the previous year.

Fluctuating Logistics Costs

- While international shipping costs decreased slightly compared to 2023, domestic logistics costs remained high, adding to product prices.

Focus on Value-Added Production

- Value-added products such as cashew milk, cashew butter, and roasted cashews gained significant attention in the international market, contributing to the increased kernel prices.

3. Domestic Cashew Production

Vietnam’s raw cashew production reached 420,000 tons, a modest 2% increase compared to 2023, supported by favorable weather and high-yield cashew varieties.

4. International Collaboration

Vietnam signed several cooperation agreements with key raw cashew suppliers such as Ivory Coast and Ghana, ensuring a stable supply chain and strengthening global value chains.

5. Sustainable Production Practices

In 2024, many Vietnamese cashew enterprises adopted international sustainability standards such as Rainforest Alliance and Fair Trade. These efforts focus on improving product quality, protecting the environment, and supporting local farming communities.

6. Logistics and Supply Chain Optimization

While volatile international shipping costs posed challenges, Vietnam made significant progress by expanding direct shipping routes to key markets such as the USA and the EU, reducing logistics pressure for exporters.

7. Expanding New Markets

Vietnam successfully penetrated emerging markets like Russia, South Korea, and the Middle East. Notably, exports to Russia rose by 15%, showcasing resilience despite geopolitical challenges.

8. Global Promotion Campaign

The Vietnam Cashew Association (VINACAS) launched a global branding campaign under the slogan: “Vietnam Cashew – Your Trusted Choice,” emphasizing the superior quality and leadership of Vietnamese cashew products in the global market.

Challenges in 2024

Despite its achievements, the Vietnamese cashew industry faced several challenges:

- Reliance on Raw Cashew Imports: Domestic production remains insufficient to meet processing demands, leading to dependency on imports from Cambodia and African countries.

- Fluctuating Logistics Costs: High shipping costs continued to impact profit margins.

- Competitive Markets: Intense competition from other cashew-exporting countries requires Vietnam to innovate and sustain its global edge.

Prosi Thăng Long’s Role in 2024

Prosi Thăng Long contributed significantly to this success, exporting 8,238 tons of cashews, representing 1.08% of the national market share. By delivering high-quality products and adhering to sustainable practices, Prosi Thăng Long has reinforced Vietnam’s standing as the premier source for cashews globally.

Conclusion and Outlook

2024 has been a transformative year for Vietnam’s cashew industry, with growth driven by strategic market expansion, sustainable practices, and international collaboration. Looking ahead, the focus on enhancing production efficiency, diversifying markets, and promoting sustainability will ensure Vietnam maintains its leadership in the global cashew market.

Prosi Thăng Long remains committed to supporting this vision, delivering premium products, and driving the industry’s continued success.

For more information about our products and services, please contact our sales team or visit our product catalog section.

#ProsiThangLong #Prosi #GlobalTrade #VietnamSpices #VietnamNuts #Pepper #Cashew #Cinnamon #Coconut #StarAnise #VietnamExporter

——————————-

𝐏𝐫𝐨𝐬𝐢 𝐓𝐡𝐚𝐧𝐠 𝐋𝐨𝐧𝐠 – 𝐒𝐩𝐢𝐜𝐞𝐬 𝐚𝐧𝐝 𝐍𝐮𝐭𝐬 𝐕𝐢𝐞𝐭𝐧𝐚𝐦 𝐌𝐚𝐧𝐮𝐟𝐚𝐜𝐭𝐮𝐫𝐞𝐫 𝐚𝐧𝐝 𝐄𝐱𝐩𝐨𝐫𝐭𝐞𝐫

𝐀𝐝𝐝𝐫𝐞𝐬𝐬: 4th Floor, Kim Anh Building, No 78 Duy Tan, Cau Giay, Ha Noi

𝐄𝐦𝐚𝐢𝐥: Sales@prosi.com.vn

𝐎𝐟𝐟𝐢𝐜𝐞 𝐇𝐨𝐭𝐥𝐢𝐧𝐞: (+84) 9858 17797

𝐘𝐨𝐮𝐫 𝐭𝐫𝐮𝐬𝐭𝐞𝐝 𝐩𝐚𝐫𝐭𝐧𝐞𝐫 𝐢𝐧 𝐩𝐫𝐞𝐦𝐢𝐮𝐦 𝐬𝐩𝐢𝐜𝐞𝐬 𝐚𝐧𝐝 𝐧𝐮𝐭𝐬

Vietnam Pepper Market Overview 2024: A Year of Growth and Transformation

Record-Breaking Performance Despite Challenges

The Vietnamese pepper industry demonstrated remarkable resilience in 2024, achieving substantial revenue growth despite volume challenges. With total exports reaching 250,600 tons and generating $1.318 billion USD, the sector showcased its ability to adapt to changing market dynamics and capitalize on favorable price conditions.

Strong Export Performance

Vietnam’s pepper exports in 2024 tell a compelling story of value over volume. While export volume saw a modest 5.1% decrease, revenue surged by an impressive 45.4% year-over-year. This success was driven by significant price increases across both black and white pepper varieties:

- Black pepper exports totaled 220,269 tons, valued at $1.117 billion USD, with average prices reaching $5,154/ton—a 49.7% increase from 2023

- White pepper exports reached 30,331 tons, generating $200.6 million USD, with prices averaging $6,884/ton—up 38.9% from the previous year

Market Leadership and Innovation

In the competitive landscape of pepper exports, several companies demonstrated exceptional performance. Olam Vietnam maintained its position as the market leader, handling 27,800 tons and capturing 11.1% market share with remarkable growth of 36.9% year-over-year.

Notable achievements were also recorded by other major players:

- Phúc Sinh processed 22,293 tons, achieving 41.1% growth

- Nedspice Vietnam handled 20,420 tons, showing steady growth of 6.4%

- Haprosimex JSC managed 17,899 tons, displaying impressive growth of 63.8%

Global Market Dynamics

The United States reinforced its position as Vietnam’s premier pepper market, importing a record-breaking 72,311 tons—representing 28.9% of total exports and marking a 33.2% increase from 2023. This achievement surpassed the previous record set in 2021 of 59,778 tons.

Other significant markets showed strong growth:

- UAE imports increased by 35.1% to 16,391 tons

- German market grew by 58.2% to 14,580 tons

- Netherlands showed robust growth of 35.2% to 10,745 tons

Price Trends and Market Conditions

The domestic market experienced significant price movements throughout 2024:

- Early 2024 saw prices climb to 92,500–95,000 VND/kg

- A peak was reached in September at 153,000–154,000 VND/kg

- The market stabilized by November at 140,000–141,000 VND/kg

Commitment to Sustainability

The industry has shown increasing commitment to sustainable practices, responding to global market demands for environmentally responsible production. This shift encompasses:

- Implementation of advanced food safety standards

- Adoption of eco-friendly farming methods

- Focus on product quality enhancement

Looking Forward

As we move forward, the Vietnamese pepper industry continues to demonstrate its ability to adapt and thrive in a changing global marketplace. The sector’s focus on quality, sustainability, and market responsiveness positions it well for continued success.

About Prosi Thăng Long

As a key player in the Vietnamese pepper industry, Prosi Thăng Long continues to maintain its position as a reliable supplier of high-quality pepper products. In 2024, the company exported 5,726 tons of pepper, demonstrating its commitment to meeting international market demands while maintaining stringent quality standards.

For more information about our products and services, please contact our sales team or visit our product catalog section.

#ProsiThangLong#Prosi#GlobalTrade#VietnamSpices#VietnamNuts#Pepper#Cashew#Cinnamon#Coconut#StarAnise#VietnamExporter

——————————-

𝐏𝐫𝐨𝐬𝐢 𝐓𝐡𝐚𝐧𝐠 𝐋𝐨𝐧𝐠 – 𝐒𝐩𝐢𝐜𝐞𝐬 𝐚𝐧𝐝 𝐍𝐮𝐭𝐬 𝐕𝐢𝐞𝐭𝐧𝐚𝐦 𝐌𝐚𝐧𝐮𝐟𝐚𝐜𝐭𝐮𝐫𝐞𝐫 𝐚𝐧𝐝 𝐄𝐱𝐩𝐨𝐫𝐭𝐞𝐫

![]() 𝐀𝐝𝐝𝐫𝐞𝐬𝐬: 4th Floor, Kim Anh Building, No 78 Duy Tan, Cau Giay, Ha Noi

𝐀𝐝𝐝𝐫𝐞𝐬𝐬: 4th Floor, Kim Anh Building, No 78 Duy Tan, Cau Giay, Ha Noi

![]() 𝐄𝐦𝐚𝐢𝐥: Sales@prosi.com.vn

𝐄𝐦𝐚𝐢𝐥: Sales@prosi.com.vn

![]() 𝐎𝐟𝐟𝐢𝐜𝐞 𝐇𝐨𝐭𝐥𝐢𝐧𝐞: (+84) 9858 17797

𝐎𝐟𝐟𝐢𝐜𝐞 𝐇𝐨𝐭𝐥𝐢𝐧𝐞: (+84) 9858 17797

𝐘𝐨𝐮𝐫 𝐭𝐫𝐮𝐬𝐭𝐞𝐝 𝐩𝐚𝐫𝐭𝐧𝐞𝐫 𝐢𝐧 𝐩𝐫𝐞𝐦𝐢𝐮𝐦 𝐬𝐩𝐢𝐜𝐞𝐬 𝐚𝐧𝐝 𝐧𝐮𝐭𝐬

Vietnam’s Cashew Industry: A Remarkable Growth Story in 2024

The Vietnamese cashew industry has demonstrated remarkable resilience and growth throughout 2024, strengthening its position as a global leader through strategic international partnerships and dynamic export performance. Here’s a comprehensive overview of the industry’s achievements and key developments.

Major Cashew Suppliers to Vietnam

Vietnam’s total cashew nut imports reached an impressive 2,385,252.67 tons, valued at $2.96 billion. Cambodia emerged as the leading supplier, contributing 782,000 tons of raw cashews worth approximately $1.1 billion. The Ivory Coast secured the second position with over 597,000 tons, valued at more than $720 million. Other markets collectively supplied more than 1,000,000 tons, reaching a value of $1.2 billion.

Outstanding Export Growth

By November 2024, Vietnam’s cashew exports had reached 711,500 tons, marking a significant year-over-year increase of 22.2% in volume and 30.7% in export value compared to 2023. The total export value reached an impressive $4.24 billion, highlighting Vietnam’s competitive advantage in the global market.

Major Export Markets

Vietnam’s cashew exports have found strong demand across several key markets:

- United States: Leading the export destinations with 147,000 tons valued at $866 million, representing 20.6% of total exports

- China: Following closely with 107,000 tons worth $616 million, accounting for 15.06% of exports

- EU and Other Markets: Dominating with a 64.33% share, totaling 457,000 tons and generating $2.75 billion in value

Industry Leaders

Vietnam’s cashew export sector is led by several prominent companies, including Olam, Long Son, Hoang Son, Thao Nguyen, Intersnack Cashew Vietnam, and Loc Viet Cuong. Notably, Prosi maintains its strong position among Vietnam’s top 10 cashew exporters.

Industry Dynamics

Despite its global leadership, Vietnam’s domestic cashew production cannot fully meet its processing demands. The country heavily relies on imports from Cambodia, Ivory Coast, Ghana, and other African nations to sustain its cashew processing industry.

Key Takeaways

The Vietnamese cashew industry continues to demonstrate robust growth despite domestic production challenges. Strategic import operations and strong export performance have reinforced Vietnam’s global leadership in the cashew market. The impressive growth in both volume and value underscores Vietnam’s significant contribution to the global supply chain.

Published by Prosi Thang Long – Your Trusted Partner in Global Cashew Trade

Vietnam Star Anise Export Report (January – August 2024)

In the first eight months of 2024, Vietnam’s star anise exports faced several challenges, with both export volume and revenue experiencing declines. By the end of August, Vietnam had exported 9,831 tons of star anise, generating a total export value of 47.3 million USD. This represents a 1.7% decrease in export volume and a 17.8% drop in revenue compared to the same period in 2023. The disparity between volume and revenue suggests that the average price of star anise has declined, possibly due to global economic conditions or shifts in demand.

Market Performance Breakdown

Despite the overall decline in exports, certain markets showed significant growth, underscoring the ongoing demand for Vietnamese star anise:

- India: Vietnam’s largest market for star anise, India imported 6,083 tons, which is 61.9% of Vietnam’s total star anise exports. This volume represents a 6.3% increase compared to the same period last year, reflecting India’s growing demand for this spice in both culinary and medicinal applications.

- United States: The U.S. imported 694 tons of star anise from Vietnam, a 8.4% increase year-on-year. Although the volume remains relatively small, the U.S. market continues to show steady growth, driven by the increasing use of star anise in food, beverages, and essential oils.

- Taiwan: One of the most notable developments in 2024 has been the 168.8% surge in exports to Taiwan, reaching 301 tons. This sharp increase indicates Taiwan’s rising demand for star anise, possibly driven by changes in food consumption trends or increased use in traditional remedies.

Prosi Thăng Long – The Market Leader

Prosi Thăng Long has solidified its position as Vietnam’s largest star anise exporter, holding nearly 20% of the market share. The company exported 1,805 tons, an impressive 12.1% increase compared to the same period in 2023. This growth is significant in light of the overall market downturn, showcasing Prosi Thăng Long’s ability to maintain strong customer relationships, ensure product quality, and adapt to market fluctuations.

As the leader in Vietnam’s star anise exports, Prosi Thăng Long’s consistent growth has been attributed to several factors:

- Strong operational capacity: The company has a well-established supply chain and state-of-the-art processing facilities that enable it to meet growing demand efficiently.

- Focus on premium quality: By emphasizing high-quality products that meet international standards, Prosi Thăng Long has gained the trust of its global customers.

- Diverse export markets: Prosi Thăng Long exports to a wide range of markets, which helps mitigate risks associated with economic downturns in specific regions.

Competitive Landscape

Several other Vietnamese exporters contributed to the country’s overall star anise exports. However, many of them experienced fluctuations in their export performance:

- Nedspice Vietnam: The second-largest exporter, Nedspice, exported 622 tons, but saw a 35.9% decrease from the previous year. This decline suggests that Nedspice may be facing challenges such as supply chain disruptions or reduced demand from key markets.

- Tuấn Minh: With an export volume of 526 tons, Tuấn Minh achieved a 25.8% growth, reflecting its successful market expansion and stronger foothold in niche markets.

- Senspices Vietnam: This exporter saw solid growth with 378 tons exported, marking a 23.5% increase. Senspices has likely capitalized on growing demand in regions where star anise is increasingly used in both food and pharmaceutical industries.

- Hồng Sơn Vietnam: With 334 tons exported, Hồng Sơn saw a 1.5% increase. While modest, this growth demonstrates stability in its export operations, even in a challenging market.

Industry Outlook

The star anise export market is expected to face continued fluctuations in the coming months due to several factors, including:

- Global economic conditions: As inflation rates and economic instability impact consumer spending in major markets, demand for star anise could be affected.

- Supply chain challenges: Disruptions caused by logistical bottlenecks and fluctuating transportation costs may continue to influence export volumes and revenues.

- Emerging markets: While established markets such as India and the U.S. remain strong, emerging markets like Taiwan are showing significant potential for growth, which could provide new opportunities for Vietnamese exporters.

Conclusion

Despite the overall decline in Vietnam’s star anise exports, Prosi Thăng Long has not only maintained but strengthened its leadership position in the market. The company’s growth, even in a challenging economic environment, reflects its operational resilience and ability to meet global demand with high-quality products. Moving forward, Prosi Thăng Long is well-positioned to capitalize on new market opportunities and continue driving the success of Vietnam’s star anise industry.

#ProsiThangLong#Prosi#GlobalTrade#VietnamSpices#VietnamNuts#Pepper#Cashew#Cinnamon#Coconut#StarAnise#VietnamExporter

——————————-

𝐏𝐫𝐨𝐬𝐢 𝐓𝐡𝐚𝐧𝐠 𝐋𝐨𝐧𝐠 – 𝐒𝐩𝐢𝐜𝐞𝐬 𝐚𝐧𝐝 𝐍𝐮𝐭𝐬 𝐕𝐢𝐞𝐭𝐧𝐚𝐦 𝐌𝐚𝐧𝐮𝐟𝐚𝐜𝐭𝐮𝐫𝐞𝐫 𝐚𝐧𝐝 𝐄𝐱𝐩𝐨𝐫𝐭𝐞𝐫

![]() 𝐀𝐝𝐝𝐫𝐞𝐬𝐬: 4th Floor, Kim Anh Building, No 78 Duy Tan, Cau Giay, Ha Noi

𝐀𝐝𝐝𝐫𝐞𝐬𝐬: 4th Floor, Kim Anh Building, No 78 Duy Tan, Cau Giay, Ha Noi

![]() 𝐄𝐦𝐚𝐢𝐥: Sales@prosi.com.vn

𝐄𝐦𝐚𝐢𝐥: Sales@prosi.com.vn

![]() 𝐎𝐟𝐟𝐢𝐜𝐞 𝐇𝐨𝐭𝐥𝐢𝐧𝐞: (+84) 9858 17797

𝐎𝐟𝐟𝐢𝐜𝐞 𝐇𝐨𝐭𝐥𝐢𝐧𝐞: (+84) 9858 17797

𝐘𝐨𝐮𝐫 𝐭𝐫𝐮𝐬𝐭𝐞𝐝 𝐩𝐚𝐫𝐭𝐧𝐞𝐫 𝐢𝐧 𝐩𝐫𝐞𝐦𝐢𝐮𝐦 𝐬𝐩𝐢𝐜𝐞𝐬 𝐚𝐧𝐝 𝐧𝐮𝐭𝐬

August Pepper Market Report

Vietnam’s pepper industry has experienced a significant surge in export earnings, increasing by 40.8% year-on-year to reach 764.2 million USD in the first seven months of this year, according to the Vietnam Pepper and Spice Association (VPSA). This remarkable growth has occurred despite a slight 2.2% decline in export volume. The rise in global pepper prices has been a key driver of this increase, with the US leading as Vietnam’s top pepper importer, purchasing 43,349 tonnes, which marks a 48.4% increase from the previous year and accounts for 26.4% of the market share.

In July alone, Vietnam exported 21,771 tonnes of pepper, earning 129.9 million USD, a 43.7% increase in volume and a 128.9% increase in value compared to the same period last year. This includes 19,371 tonnes of black pepper and 2,400 tonnes of white pepper. The total export volume from January to July reached 164,357 tonnes, comprising 145,330 tonnes of black pepper and 19,027 tonnes of white pepper.

To sustain this positive momentum, VPSA Chairwoman Hoang Thi Lien emphasized the need to stabilize pepper cultivation areas while enhancing product quality and diversifying high-value processed products. She also recommended that farmers adopt international standards concerning chemical residues, cultivation practices, pest control, and preservation methods suited to regional climatic conditions. Developing new pepper varieties with higher yields, better quality, and disease resistance is crucial.

On the global stage, the International Pepper Community (IPC) reported mixed market reactions. For instance, while Indian and Sri Lankan pepper prices remained stable, Indonesia saw an increase in its domestic and international pepper prices, driven by a 1% appreciation of the Indonesian Rupiah against the US dollar. Meanwhile, Malaysia experienced a 3% increase in the Ringgit’s value, contributing to higher pepper prices as the country entered its harvest season. In contrast, Vietnam’s domestic and export pepper prices saw a decline, and Brazil’s black pepper prices also fell, while pepper prices in Cambodia and China remained stable.

As of August 17th, the domestic pepper price in Vietnam ranged from 139,000 to 140,000 VND/kg, showing an increase of 2,000 to 2,500 VND/kg from the previous day. The latest trade data also indicated that Vietnam’s black pepper prices were at 5,800 USD/ton for 500 g/l type and 6,200 USD/ton for 550 g/l type, while white pepper was priced at 8,500 USD/ton.

Looking ahead, the global pepper market is expected to reach 1 billion USD this year, with Vietnamese exporter Phuc Sinh maintaining an 8% share of the global market. The company’s export volume has grown by 40%, with average export prices doubling compared to the same period last year. In Vietnam, domestic pepper prices have risen to 140,000 VND/kg, a 1.75-fold increase from earlier this year, reaching up to 158,000 VND/kg at their peak, driven by the scarcity of supply.

As the market evolves, leveraging digital technology for production management, traceability, and market access will be essential. Additionally, promoting cooperatives and production groups will help strengthen the supply chain and benefit exporters, ensuring that Vietnam remains a key player in the global pepper industry.

#ProsiThangLong#Prosi#GlobalTrade#VietnamSpices#VietnamNuts#Pepper#Cashew#Cinnamon#Coconut#StarAnise#VietnamExporter

——————————-

𝐏𝐫𝐨𝐬𝐢 𝐓𝐡𝐚𝐧𝐠 𝐋𝐨𝐧𝐠 – 𝐒𝐩𝐢𝐜𝐞𝐬 𝐚𝐧𝐝 𝐍𝐮𝐭𝐬 𝐕𝐢𝐞𝐭𝐧𝐚𝐦 𝐌𝐚𝐧𝐮𝐟𝐚𝐜𝐭𝐮𝐫𝐞𝐫 𝐚𝐧𝐝 𝐄𝐱𝐩𝐨𝐫𝐭𝐞𝐫

![]() 𝐀𝐝𝐝𝐫𝐞𝐬𝐬: 4th Floor, Kim Anh Building, No 78 Duy Tan, Cau Giay, Ha Noi

𝐀𝐝𝐝𝐫𝐞𝐬𝐬: 4th Floor, Kim Anh Building, No 78 Duy Tan, Cau Giay, Ha Noi

![]() 𝐄𝐦𝐚𝐢𝐥: Sales@prosi.com.vn

𝐄𝐦𝐚𝐢𝐥: Sales@prosi.com.vn

![]() 𝐎𝐟𝐟𝐢𝐜𝐞 𝐇𝐨𝐭𝐥𝐢𝐧𝐞: (+84) 9858 17797

𝐎𝐟𝐟𝐢𝐜𝐞 𝐇𝐨𝐭𝐥𝐢𝐧𝐞: (+84) 9858 17797

𝐘𝐨𝐮𝐫 𝐭𝐫𝐮𝐬𝐭𝐞𝐝 𝐩𝐚𝐫𝐭𝐧𝐞𝐫 𝐢𝐧 𝐩𝐫𝐞𝐦𝐢𝐮𝐦 𝐬𝐩𝐢𝐜𝐞𝐬 𝐚𝐧𝐝 𝐧𝐮𝐭𝐬